Inventory, Softening Demand Cooling Pace of Home Sales

[ad_1]

In accordance to the Realtor.com Regular Housing Tendencies Report, new information suggests that the U.S. housing provide is preparing to rebound, as lively listings posted the smallest calendar year-in excess of-calendar year declines —down just -12.2% given that December 2019.

Inventory enhancements had been led by will increase in the share of mid-sized homes, that means a lot more listings may possibly be accessible to family members hunting to update from their starter homes, probably ensuing in an uptick in to start with-time obtaining options.

“April details implies a positive convert of occasions is on the horizon for weary customers: If the trends we’re viewing now hold true, we could probably see 12 months-in excess of-yr inventory advancement in the following couple months,” reported Danielle Hale, Chief Economist for Real estate agent.com. “The essential to this development will be the continuation of softening consumer level of competition and an growing quantity of sellers placing households on the market place. Even though residence shoppers are continue to looking for reduction from document-substantial inquiring selling prices and all-time lower offer, when as opposed to the earlier two-plus several years of double-digit annual stock declines, an imminent rebound is welcome information – a actual estate refresh, if you will. There is certainly a lengthy uphill climb to harmony, but it commences with heading in the appropriate path, and April information demonstrates a whole lot of guarantee.”

In April, the U.S. offer of for-sale households showed several indications of accelerated enhancements, as greater house loan fees slash into some buyers’ flexibility to compete. Even though new listings declined calendar year-over-yr, so did the amount of residences under agreement, suggesting that softening need is cooling the intensive pace of property profits. As a consequence of these blended tendencies, the gap in active listings from very last year ongoing to shrink, led by increases in the share of mid-sized properties. This could signify more possibilities readily available to families searching to improve from and provide their starter homes, which could possibly lead to an improve in essential initial-time buying inventory.

For all customers continue to procuring, the continuation of these traits would probable signify some sooner-than-expected reduction in accessible solutions. Stock could hit annual advancement by next thirty day period and start out the extensive highway to entire recovery from COVID declines.

Critical Takeaways from 400+ Metros:

- The U.S. stock of active listings was down 12.2% 12 months-about-yr in April, an enhancement about March (-18.9%) and the smallest annual drop because December 2019 (-12.7%). Between this offer, the share of mid-sized (1,750-3,000 sq. foot) properties posted the major get, up 2.34 share factors 12 months-around-12 months (see table below).

- Nationally, pending listings ended up down 9.5% 12 months-in excess of-12 months, a likely side outcome of moderating demand on the tempo of stock turnover. These trends mirror intensifying price pressures faced by customers, with the expense of funding 80% of the common house listing up by pretty much 50% as opposed to a yr ago.

- New listings acquired some momentum in April, but ultimately ended the month marginally down below previous year’s amount (-.9%) and 13.% reduce than regular April concentrations from 2017-2019.

- As opposed to the countrywide fee, active listings declines from April 2021 were somewhat smaller in the 50 most significant metros, on typical (-10.3%), and strike beneficial territory in eight marketplaces, led by Riverside, Calif. (+23.3%), Austin, Texas (+16.5%) and Sacramento, Calif. (+11.8%).

- Seventeen metros posted calendar year-more than-calendar year gains in recently-shown homes, topped by New Orleans (+15.2%), San Antonio (+12.5%) and Denver (+11.3%).

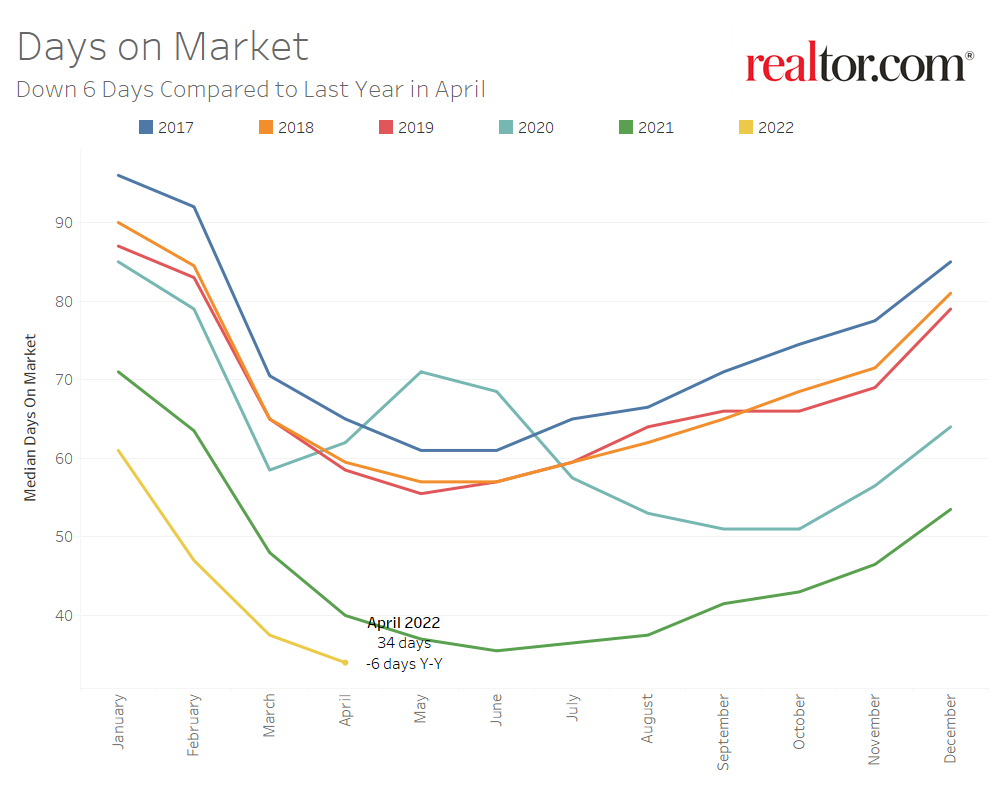

For potential buyers nevertheless in the sector, softening level of competition is presenting a lot-wanted relief from the extraordinary pace that stock is relocating as opposed to last calendar year. Homes keep on to market promptly, at a history-fast tempo in April, but the gap from past yr has been shrinking. In actuality, the yearly amount dropped by half from March. Ailments had been somewhat extra aggressive in the 50 greatest U.S. metros, all of which posted annually declines in time on marketplace. Several of the metros where by households moved swiftest compared to previous calendar year ended up in the Solar Belt region, which has turn out to be ever more well-liked with potential purchasers from other states.

In April, the normal U.S. household invested 34 days on marketplace, six times fewer than very last calendar year and beating the previous history-reduced of 36 days in June 2021. Typical time on industry in the 50 biggest U.S. metros was 28 times, 6 times much less than past 12 months. Regionally, the South posted the most important year-above-12 months declines in time on current market (-9 days), adopted by the West (-5 times).

At the metro-level, homes moved at the quickest calendar year-in excess of-yr tempo were in:

- Miami (-29 times)

- Louis (-15 times)

- Raleigh, North Carolina (-14 days)

- Orlando, Florida (-13 times)

- Hartford, Connecticut (-13 times)

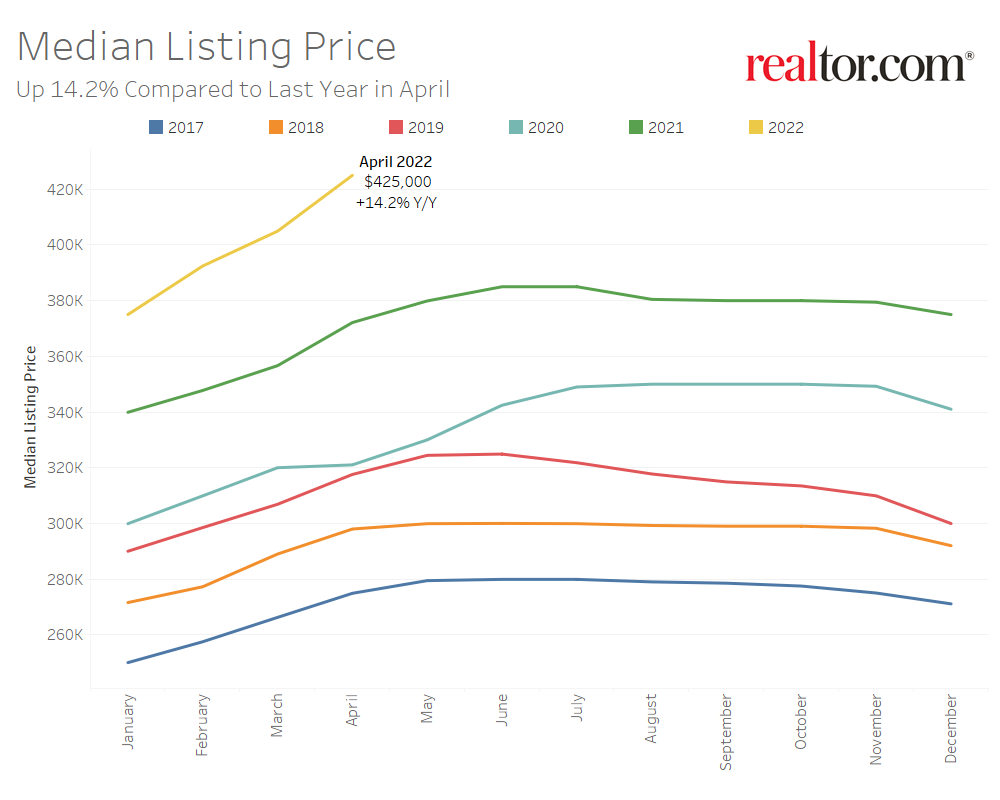

Irrespective of moderating demand from customers, the U.S. median residence selling price strike still an additional all-time substantial and accelerated more than the March annual expansion rate in April. While previously elevated, this boost may perhaps be lessen than what some dwelling consumers experienced, simply because medians can shift together with the blend of for-sale inventory.

April’s median reflects fewer big listings and much more mid-sized listings obtainable compared to a calendar year ago, with listing costs per square foot mounting at a fairly more quickly pace than the general median, but moderating slightly from the March level. In a different indicator of some customers tightening their budgets owing to amount hikes, the share of sellers generating price tag reductions increased year-over-yr nationwide and in most massive metros.

- The median nationwide home price hit a new all-time large of $425,000 in April, up 14.2% 12 months-above-yr. Though general asking rates accelerated around very last month’s pace (13.5%), the once-a-year expansion rate declined on a sq. foot basis, to 15.1% from 15.7% in March.

- Nationally, the share of properties with value reductions improved 1.3 percentage details year-more than-calendar year to 6.9%, but lagged guiding common 2017 to 2019 ranges (-9 percentage details).

- In April, listing price ranges in the 50 premier U.S. metros grew at a solitary-digit rate (+9.5%), on average. On the other hand, asking charges for each sq. foot greater by double-digits (+12.3%) and nearer to the countrywide rate overall.

- Western (+14.5%) and southern (+14.1%) metros topped the checklist of largest year-more than-calendar year rate improves, up 22% or far more in Miami, Las Vegas, Orlando, Fla., Tampa, Fla., Austin, Nashville, Tenn., Jacksonville, Fla. and Phoenix.

- In 40 of the 50 premier metros, the share of listings to which selling price reductions were manufactured in the thirty day period of April improved calendar year-in excess of-12 months, by the most percentage details in: Austin (+6.8), Las Vegas (+5.3) and Sacramento (+4.7).

To browse the comprehensive report, including charts and methodology, click on right here.

[ad_2]

Source backlink